Accountants Scrutinize Trump’s 2005 Federal Income Taxes

![]()

By Nitin Chandra, CPA & Umesh (Mike) Jain, CPA

HOUSTON: The past few weeks have been very trying ones for our great nation. Our hearts go out to all the people of the Gulf Coast who weathered Harvey with tremendous courage; to those along the Atlantic Coast in the aftermath of Hurricane Irma and then to those who have to rebuild their lives after the devastation caused by Hurricanes Irma and Maria in Puerto Rico. Now, there is this horrific massacre in Las Vegas leaving 57 dead and 519 injured.

In Houston, virtually all citizens were directly impacted by the aftermath of Hurricane Harvey – the flooding we witnessed did not discriminate by class, creed, socio-economic status or structure. Entire neighborhoods were ravaged as homes, places of worship, schools, social gathering spots and workplaces were lost to the devastation. In the days since Harvey, we have been incredibly fortunate and grateful to have the full support of our nation behind us as we help rebuild our great city.

During those same weeks, most CPAs across the United States were preoccupied with a different kind of hurricane – the annual September 15th and the upcoming October 15th tax filing deadlines. At our firm, the deadlines this year were especially challenging because we were busy gathering data, completing returns while simultaneously bracing for Harvey for the entire week of August 28th. The IRS extended the filing and payment deadlines for federal returns and taxes only after Harvey left the Greater Houston area.

Unable to drive to our office, we were forced to take a break from preparing and reviewing our clients’ returns. Instead, this allowed us to focus our attention to analyze President Donald Trump’s recently leaked 2005 Federal Income Tax Return. Independent of political beliefs, as tax professional and taxpayers, we found the joint return of Donald J. Trump and Melania Knavs very disappointing, interesting and troubling.

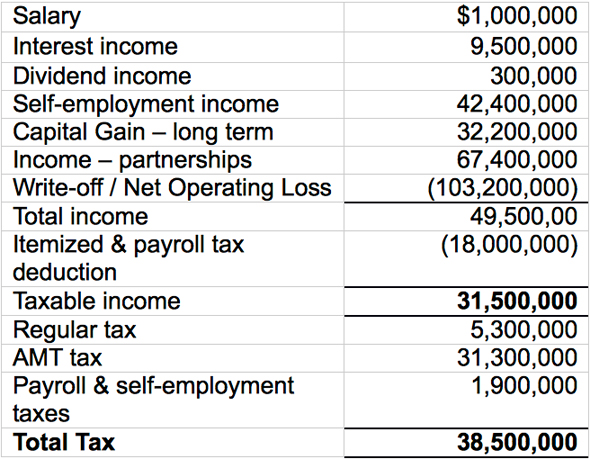

Disappointing: Upon close scrutiny of the President’s tax return, we were disappointed to discover that Jain and Jain, P.C. could not have prepared this return because our tax software cannot accommodate numbers greater than $99 Million. The President had a write-off and use of Net Operating loss of $103 million in that year.

Interesting and Troubling. After accounting for write-offs and losses, President Trump’s joint 2005 return reported total taxable income of $31.5 million. There is no question that the President and First Lady are in the top 1% wealth bracket of Americans. What is deeply troubling about their return is that their tax bill of $38.5 million is greater than the reported taxable income. This is because they paid $5.3 million in regular taxes, $31.3 million in Alternative Minimum Tax (commonly known as AMT) and $1.9 million in self-employment taxes. Their tax breakdown was:

While there is not much that we (including the President) can do about the tax laws, we certainly ought to be planning for the numerous taxes that we may incur. Businesses ought to be plan around not only Regular Income Tax, but also AMT, Self-employment tax, and Obama Medicare tax. Businesses should also look at taking advantage of R&D Credits, IC-Disc, deductions for domestic manufacturers and producers as well as a host of other potential deductions and opportunities.

Jain of the Jain & Jain, P.C. is a professional accounting firm which provides Audit, Tax, and Consulting services to medium and large-size businesses and also offers tax diagnostic services to help businesses seek and realize potentially uncaptured tax savings.