Financial Education — Planning for Kids’ Education Part 2

Following up on our initial article on Education Funding for Kids, let’s take a deeper dive into EFC or Expected Family Contribution. How does EFC work and what is the impact on your child getting financial help from the college they are applying to [Scholarships or Need-Based Aid]

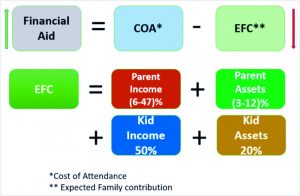

Take a look at the graphic below.

Availability of Financial Aid is determined by two primary factors – COA or Cost of Attendance and EFC or Expected Family Contribution. As mentioned in our previous article, COA is what the College Charges for the various aspects of education.

EFC is the most important determining factor in how much Need-Based Financial Aid a student receives. As the graphic shows, there are two sections that are considered – Parents and Kids, each with two subsections: Income and Assets.

Breaking things down further:

- 6-47% of Parent’s Income have an impact (varies by college)

- 3-12% of Parent’s Assets have an impact (varies by college)

- 50% of the Kid’s Income prior to entering college is considered and has a significant impact.

- 20% of the Kid’s Assets have an impact.

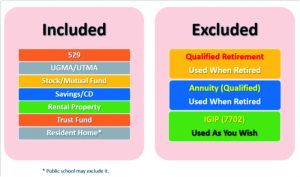

The first two subsections (Parent’s Income & Parent’s Assets) will be considered no matter what. Given that the Parent’s Income section cannot be modified (unless there is a loss of employment), a prudent way to reduce exposure in the Parent’s Assets is to move some of the Assets from the category of “Included” to “Excluded” (see graphic below). Keep in mind that there is a lookback period of 2 years on the Parent’s Income & Assets before a child is admitted to college, so any movement of assets MUST be done before this lookback period.

Excluded Assets, by definition, MUST be excluded while considering a child’s financial aid package by the college. How to reposition your assets requires time and a proper method – which is where we come in with our Consulting services.

Excluded Assets, by definition, MUST be excluded while considering a child’s financial aid package by the college. How to reposition your assets requires time and a proper method – which is where we come in with our Consulting services.

Now, what about the kid’s Income and Assets?

Many kids like to do part time jobs for experience or additional pocket money and there is nothing wrong with that generally – except when it comes to applying for Need-Based Aid. Colleges want their money and will expect the kid to fork over 50% (above a certain threshold) of their pre-college income towards the EFC. Our advice, if there is no critical need for your child to earn the extra money, dissuade them from doing so. Instead advise them to do as much Volunteering as possible in their school years. This builds a solid resume and has a greater impact towards admissions.

Lastly, your kid’s assets. In our zeal to provide a financial cushion for our kids, Parents and Grandparents (and other relatives) will provide financial or other assets to kids. This falls under the UGMA/UTMA framework of Included Assets and becomes detrimental to a kid’s financial aid prospects since 20% of these assets are considered part of the EFC. One strategy is to transfer these assets to the kids after they are out of college and in the workforce.

Hopefully, this discussion gets your mind working towards a better solution to finance your kid’s education. If you have some time before your child goes to college, get with us and we can plan out some specific strategies for you to reduce the impact of EFC.

To conclude, my team and I are here to educate you on topics pertaining to personal finance, show you how to avail of some of these financial vehicles, and help you position yourselves with these vehicles. We are FEFAF – Families Educating Families About Financial success. Let our fantastic team of Financial Mentors expand your vision! Send in your questions or comments to me at amfinins@gmail.com or text me at 832.723.9555. Let’s talk and discuss your financial goals and fill in the gaps in your financial education and planning.

A long-time resident of Houston, Ash is also a proud UofH Alumni with a background in Computer Science. This expertise developed into an IT Security & Managed Services Business which he has successfully run for the last 13 years. Ash is a constant learner and teacher, expanding his business expertise into Real Estate and lately into the remarkable area of Financial Education. This – Educating families about Finance and the correct vehicles for growth, protection, and Tax Benefit strategies – is his absolute passion.

A long-time resident of Houston, Ash is also a proud UofH Alumni with a background in Computer Science. This expertise developed into an IT Security & Managed Services Business which he has successfully run for the last 13 years. Ash is a constant learner and teacher, expanding his business expertise into Real Estate and lately into the remarkable area of Financial Education. This – Educating families about Finance and the correct vehicles for growth, protection, and Tax Benefit strategies – is his absolute passion.

Salil Patil is an Electrical Engineer by profession getting his MS & MBA from Lamar University. He currently works in Oil & Gas as a Senior Instrumentation Manager. Given his technical skills and phenomenal number crunching abilities, he dove headfirst into the area of Financial Education when the opportunity presented itself and has now made it his Plan B in life. He is the passionate team lead of the FEFAF group.

Salil Patil is an Electrical Engineer by profession getting his MS & MBA from Lamar University. He currently works in Oil & Gas as a Senior Instrumentation Manager. Given his technical skills and phenomenal number crunching abilities, he dove headfirst into the area of Financial Education when the opportunity presented itself and has now made it his Plan B in life. He is the passionate team lead of the FEFAF group.